Models in Neuroscience

Contents

9. Models in Neuroscience¶

9.1. NSCI 801 - Quantitative Neuroscience¶

Gunnar Blohm

9.1.1. Outline¶

Models in scientific discovery

Usefulness of models

Model fitting

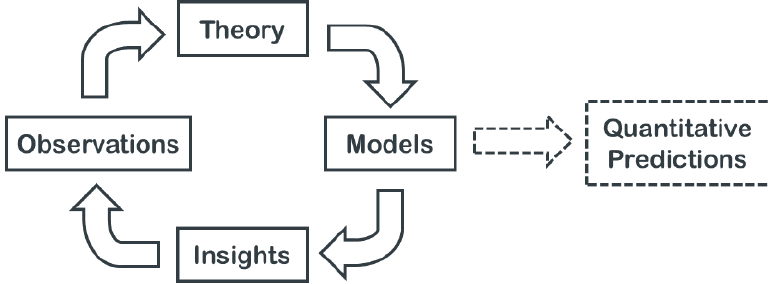

9.1.2. Models in scientific discovery¶

Models help answering three potential types of questions about the brain (Dayan & Abbott, 2001)

Descriptive = What? – Compact summary of large amounts of data

Mechanistic = How? – Show how neural circuits perform complex function

Interpretive = Why? – Computations in the brain are usually performed in an optimal or nearly optimal way / Understanding optimal algorithms and their implementation to explain why the brain is designed the way it is

9.1.3. Models in scientific discovery¶

There are different levels of models (Marr)

Computational level - 1: what does the system do and why does it do these things

Algorithmic level - 2: how does the system do what it does, specifically, what representations does it use and what processes does it employ to build and manipulate the representations

Implementation level - 3: how is the system physically realised

9.1.4. Models in scientific discovery¶

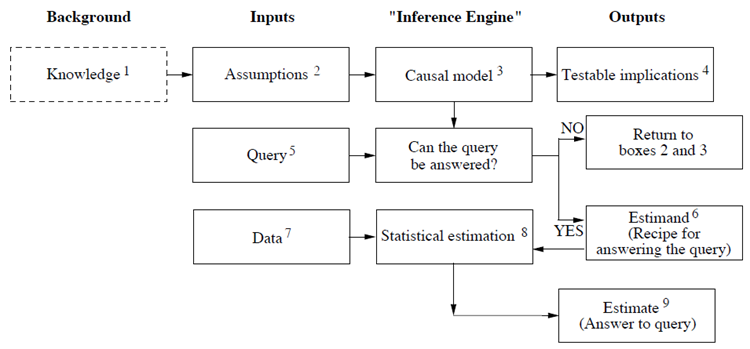

Judea Pearl (in “Book of WHY”): “the model should depict, however qualitatively, the process that generates the data: in other words, the cause-effect forces that operate in the environment and shape the data generated.”

9.1.5. Usefulness of models¶

Gain understanding

Identify hypotheses, assumptions, unknowns

Make quantitative predictions

Build brain model (stroke lesions etc)

Inspire new technologies

Design useful experiments (i.e. animal research)

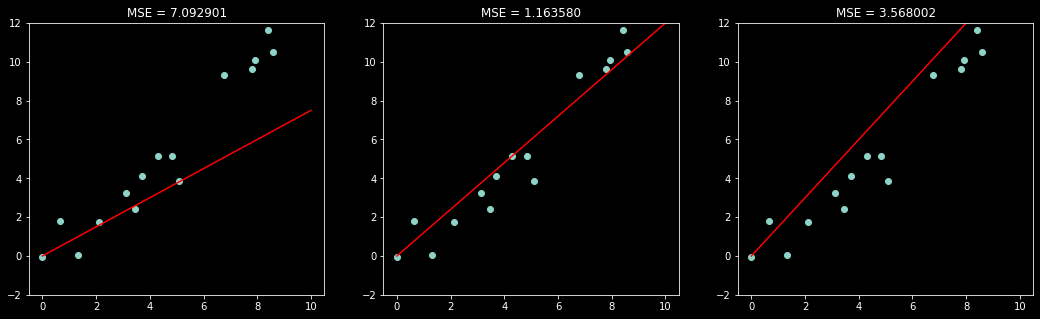

9.1.6. Model fitting 1 - MSE¶

A common method is to compute the average (mean) squared error (MSE) of the model predictions \(\hat{y_i}\) for the \(m\) true values \(y_i\) in the data set: $\( \textrm{MSE}_{\textrm{test}} = \frac{1}{m}\sum_i(\hat{y_i}-y_i)^2\)$

Let’s try this…

9.1.7. Model fitting 1 - MSE¶

from scipy.stats import norm

import numpy as np

import matplotlib.pyplot as plt

from scipy.optimize import minimize

from mpl_toolkits.mplot3d import Axes3D

from matplotlib import cm

%matplotlib inline

np.random.seed(44)

plt.style.use('dark_background')

---------------------------------------------------------------------------

ModuleNotFoundError Traceback (most recent call last)

Input In [1], in <cell line: 1>()

----> 1 from scipy.stats import norm

2 import numpy as np

3 import matplotlib.pyplot as plt

ModuleNotFoundError: No module named 'scipy'

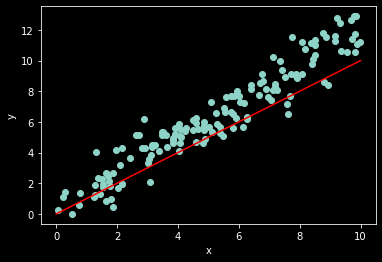

# (adapted from Ben Cuthbert's tutorial)

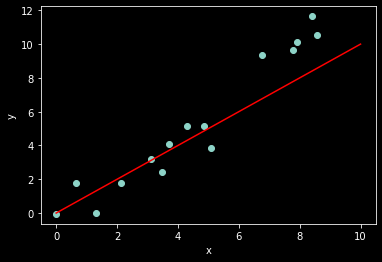

# generate some noisy data

n_samples = 15

w_true = 1.2

x = np.random.rand(n_samples)*10

noise = norm.rvs(0,1,x.shape) # the original code used uniform noise

y = w_true*x + noise

ax = plt.subplot(1,1,1)

ax.scatter(x, y)

ax.set_xlabel('x')

ax.set_ylabel('y')

# linear regression model (just for show)

x_axis = np.linspace(0,10,20)

w = 1 # our guess for the value of w

y_hat = w*x_axis

ax.plot(x_axis, y_hat, color='red');

In order to fit a model, we first need to define our error function:

def compute_mse(x, y, w):

"""function that computes mean squared error"""

y_hat = w*x

mse = np.mean((y - y_hat)**2)

return mse

Now let’s evaluate the MSE of three different models (values of \(w\))

w = [0.75, w_true, 1.5]

fig, ax = plt.subplots(1, 3, figsize=(18,5))

for i in range(3):

ax[i].scatter(x, y)

ax[i].plot(x_axis, w[i]*x_axis, color='red')

ax[i].set_ylim(-2,12)

ax[i].set_title('MSE = %f' % compute_mse(x,y,w[ i]));

9.1.8. Model fitting 1 - MSE¶

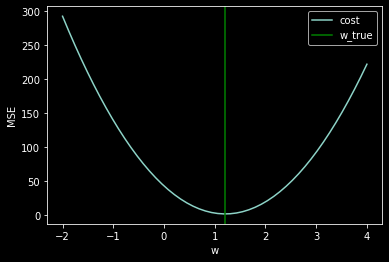

We still haven’t answered our question: How do we choose \(w\)?

The key is to think of MSE as a cost function.

n_points = 50

all_w = np.linspace(-2,4,n_points)

mse = np.zeros((n_points))

for i in range(n_points):

mse[i] = compute_mse(x, y, all_w[i])

plt.plot(all_w,mse)

plt.xlabel('w')

plt.ylabel('MSE')

plt.axvline(w_true, color='green')

plt.legend(['cost','w_true']);

How do we choose \(w\)? Minimize the cost function!

To minimize MSE, we solve for where its gradient is 0:

This is known as solving the normal equations (see Deep Learning 5.1.4 for more details).

def solve_normal_eqn(x,y):

"""Function that solves the normal equations to produce the

value of w that minimizes MSE"""

# our numpy arrays are 0-dimensional by default- for the

# transpose/dot product/inverse to work, we reshape them

m = len(x)

x = np.reshape(x, (m, 1))

y = np.reshape(y, (m, 1))

w = np.dot(np.dot(np.linalg.inv(x.T.dot(x)),x.T),y)

return w

solve_normal_eqn(x,y)

array([[1.20816968]])

And we’re done! We have just recovered \(w\) from the noisy data by analytically computing the solution to finding the minimum of the cost function!

However this only works for very few select functions, such as linear functions…

Thus: we need a more general way…

9.1.9. Model fitting 2 - MLE¶

The likelihood of the data given the model can be used directly to estimate \(\theta\) through maximum likelihood estimation (MLE): $\(\hat{\theta_{MLE}}=\underset{\theta}{\operatorname{argmax}} P(D| \theta)\)$

So practically, how do we do this?

9.1.10. Model fitting 2 - MLE¶

The likelihood of the model given the data is \(\mathcal{L}(\theta|D) = P(D|\theta)\)

Think of probability relating to possible results

Think of likelihood relating to hypotheses

Here we assume Gaussian noise; the loglikelihood is thus given by:

We now want to minimize the negative loglikelihood…

9.1.11. Model fitting 2 - MLE¶

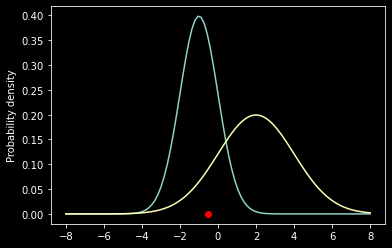

What is a likelihood?

Let’s say we have a single lonely data point \(x\) sampled from one of two candidate normal distributions \(f_1=\mathcal{N}(\theta_1)\) and \(f_2=\mathcal{N}(\theta_2)\) where \(\theta_1 = \{\mu_1,\sigma_1\}\) and \(\theta = \{\mu_2, \sigma_2\}\).

x = -0.5

mu1, sig1 = -1, 1

mu2, sig2 = 2, 2

x_axis = np.linspace(-8,8,100)

f1 = norm.pdf(x_axis, mu1, sig1)

f2 = norm.pdf(x_axis, mu2, sig2)

ax = plt.subplot(111)

ax.scatter(x, 0, color='red');

ax.plot(x_axis, f1);

ax.plot(x_axis, f2);

ax.set_ylabel('Probability density');

prob1 = norm.pdf(x, mu1, sig1)

prob2 = norm.pdf(x, mu2, sig2)

print('L(theta1|x) = %f' % prob1)

print('L(theta2|x) = %f' % prob2)

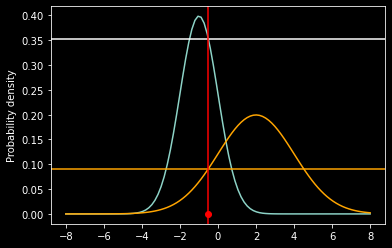

ax = plt.subplot(111)

ax.scatter(x, 0, color='red');

ax.plot(x_axis, f1);

ax.plot(x_axis, f2, color='orange');

ax.axhline(prob1)

ax.axhline(prob2, color='orange')

ax.axvline(x, color='red')

ax.set_ylabel('Probability density');

L(theta1|x) = 0.352065

L(theta2|x) = 0.091325

9.1.12. Model fitting 2 - MLE¶

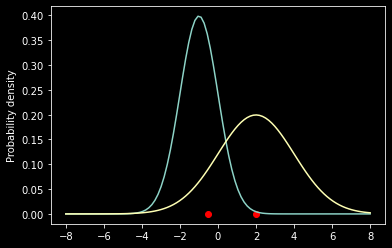

What if we now add a data point?

x = [-0.5, 2]

ax = plt.subplot(111)

ax.scatter(x, [0, 0], color='red')

ax.plot(x_axis, f1)

ax.plot(x_axis, f2)

ax.set_ylabel('Probability density')

plt.show()

prob1 = norm.pdf(x[0], mu1, sig1)*norm.pdf(x[1], mu1, sig1)

prob2 = norm.pdf(x[0], mu2, sig2)*norm.pdf(x[1], mu2, sig2)

print('L(theta1|x) = %f' % prob1)

print('L(theta2|x) = %f' % prob2)

L(theta1|x) = 0.001560

L(theta2|x) = 0.018217

9.1.13. Model fitting 2 - MLE¶

Now back to our fitting problem…

We need to define our loglikelihood function:

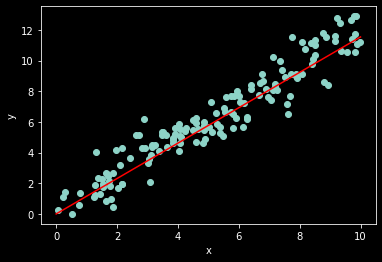

# generate some noisy data

n_samples = 150

w_true = 1.2

x = np.random.rand(n_samples)*10

noise = norm.rvs(0,1,x.shape) # the original code used uniform noise

y = w_true*x + noise

ax = plt.subplot(1,1,1)

ax.scatter(x, y)

ax.set_xlabel('x')

ax.set_ylabel('y')

# linear regression model (just for show)

x_axis = np.linspace(0,10,20)

w = 1 # our guess for the value of w

y_hat = w*x_axis

ax.plot(x_axis, y_hat, color='red');

def compute_y_hat(x, w):

"""function that computes y_hat (aka y=w0*1 + w1*x)"""

y_hat = np.dot(x,w)

return y_hat

# pad x so that matrix operation X*w gives w0 + x*w1

X = np.c_[np.ones((x.shape[0], 1)), x]

# we assume the data is normally distributed around the function defined in y_hat...

def compute_nll(x, y, w):

"""function that computes the negative log likelihood of a gaussian"""

y_hat = compute_y_hat(x, w)

sig = np.std(y-y_hat)

ll = -np.sum(norm.logpdf(y, y_hat, sig))

return ll

We’re now ready to minimize the loglikelihood function through adapting model parameters…

from scipy.optimize import minimize

# initial guess of w

w0 = np.array([0, 1])

# define a new version of our -log-likelihood that is only a function of w:

fun = lambda w: compute_nll(X, y, w)

# pass these arguments to minimize

result = minimize(fun, w0)

print(result)

# plot results

ax = plt.subplot(1,1,1)

ax.scatter(x, y)

ax.set_xlabel('x')

ax.set_ylabel('y')

# linear regression model (just for show)

x_axis = np.linspace(0,10,20)

w = result.x[1] # our guess for the value of w

y_hat = w*x_axis

ax.plot(x_axis, y_hat, color='red');

fun: 203.6943986857902

hess_inv: array([[ 0.02791486, -0.00426672],

[-0.00426672, 0.00082749]])

jac: array([1.90734863e-06, 3.81469727e-06])

message: 'Optimization terminated successfully.'

nfev: 30

nit: 6

njev: 10

status: 0

success: True

x: array([0.34100692, 1.15404339])

All done!

9.1.14. Model fitting 2 - MLE¶

In practice, we don’t want to test our model on the same data we trained it with! To avoid that we typically divide data into training set and test set. This allows for what’s called cross-validation. General procedure:

draw a random subset of your data = training data. Remaining data = test set

perform fitting procedure on training set to identify model parameters

test model performance on test set, e.g. compute loglikelihood of test set given the identified model parameters

do this many times…

If your training set is all but 1 data point, this is called leave-one-out cross-validation.

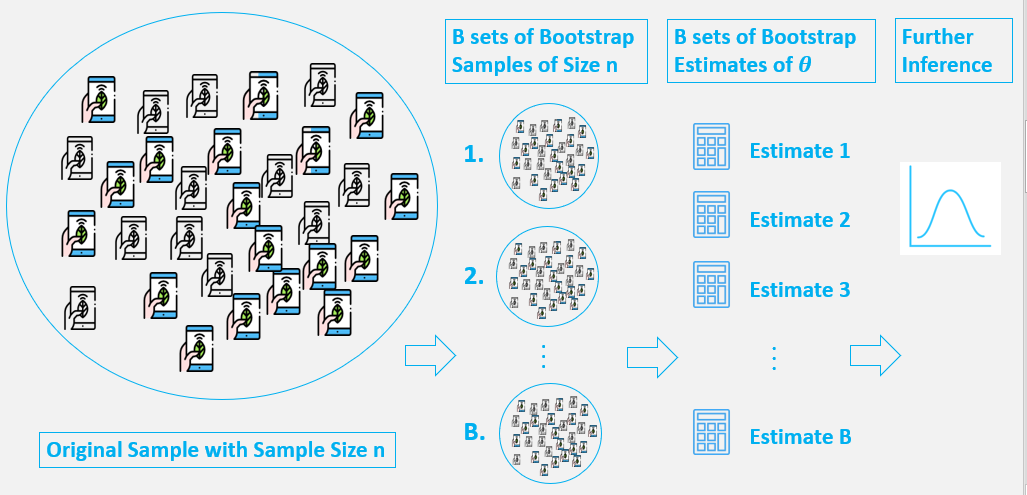

9.1.15. Model fitting - bootstrap¶

Bootstrapping is similar cross-validation, but the boostrap sample is chosen in a specific way to obtain meaningful statistics on the estimated parameters.

Bootstrapping is a test/metric that relies on random sampling with replacement. As a result, we can estimate properties of estimators (e.g. fit parameters).

Assumption: the limited data available is representative of the population data.

Advantage: no prior knowledge or assumption about the data sampling process!

9.1.17. Model fitting - bootstrap¶

Bootstrap comes in handy when there is no analytical form or normal theory to help estimate the distribution of the statistics of interest, since bootstrap methods can apply to most random quantities. Here is how it works:

randomly resample your data with replacement

perform estimation on resampled data, e.g. compute mean, perform model fit, etc

repeat many times, e.g. \(N=1000\)

compute bootstrap distribution

Result: empirical percentiles (\(\alpha\)/2) of bootstrap distribution form confidence interval over parameters with confidence level \(\alpha\), i.e. \((\theta^*_{\alpha/2}, \theta^*_{1-\alpha/2})\)

Let’s do it!

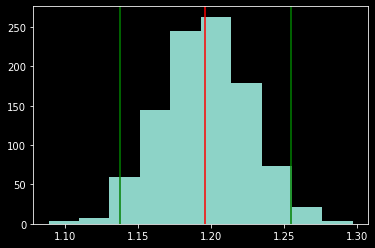

# generate some noisy data

n_samples = 150

w_true = 1.2

x = np.random.rand(n_samples)*10

noise = norm.rvs(0,1,x.shape) # the original code used uniform noise

y = w_true*x + 1*noise

boot_est = []

for _ in range(1000):

# chose a random sample of our data with replacement

bootind = np.random.choice(list(range(0,n_samples-1)),size=n_samples, replace=True)

xb = x[bootind]

yb = y[bootind]

# append 1s

Xb = np.c_[np.ones((xb.shape[0], 1)), xb]

# fit model

w0 = np.array([0, 0])

fun = lambda w: compute_nll(Xb, yb, w)

result = minimize(fun, w0)

# save results

boot_est.append(result.x[1])

# plot bootstrap distribution

plt.hist(boot_est)

# confidence level

alp = 0.05

# compute percentiles

est_low = np.percentile(boot_est, 100*alp/2)

est_high = np.percentile(boot_est, 100*(1-alp/2))

est_median = np.percentile(boot_est, 50)

est_mean = np.mean(boot_est)

est_std = np.std(boot_est)

plt.axvline(est_low, color='green')

plt.axvline(est_high, color='green')

plt.axvline(est_median, color='red')

print([est_low, est_median, est_high])

print([est_mean, est_std])

[1.1376369217837263, 1.1958713507549792, 1.2546932636792674]

[1.1955797053496076, 0.029987463824238652]

9.1.18. Model comparison: how to chose the best model?¶

use Bayes Factor (see last lecture)

compare MSE after k-fold cross-validation

use Akaike’s Information Criterion (AIC)

Always split your dataset into training data and test data!

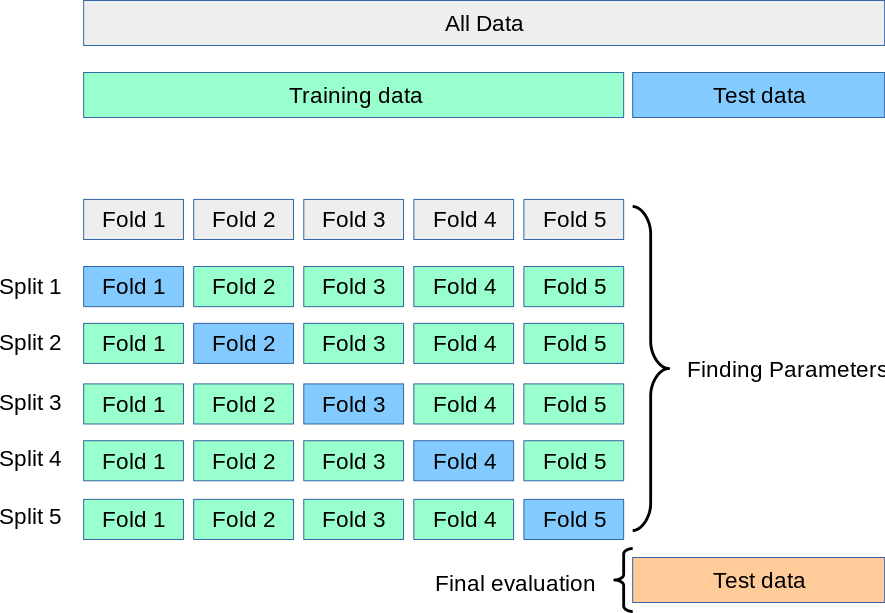

9.1.19. k-fold cross-validation¶

if you want to do that, check out the from scikit-learn tutorial or the Neuromatch Academy tutorial on model fitting (especially tutorial 6)

9.1.20. Akaike Information Criterion (AIC)¶

Estimates how much information would be lost if the model predictions were used instead of the true data.

AIC strives for a good tradeoff between overfitting and underfitting by taking into account the complexity of the model and the information lost. AIC is calculated as:

with:

K: number parameters in the model

\(\log(L)\): loglikelihood of data given your best model paremeters

Note: smallest AIC values are best! (see Wikipedia page for more info)

We can now do model comparison by computing the following relative probability that ith model minimizes the (estimated) information loss: